Quick Overview

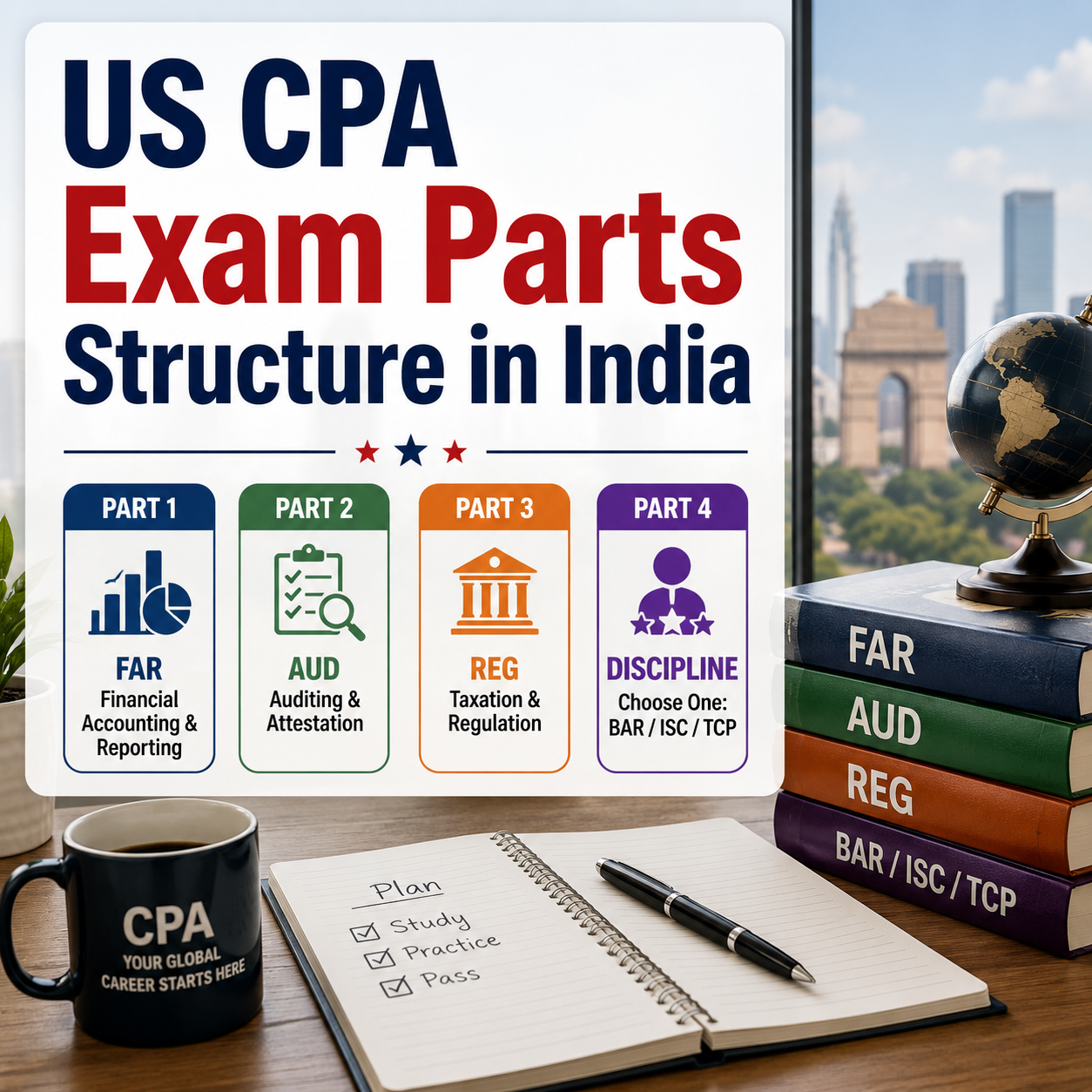

The US CPA Exam is built from four parts. Three are compulsory Core sections that every candidate sits for. And the fourth is a Discipline section you choose yourself. Here is the shape of it at a glance:

- Part 1 – FAR (Financial Accounting and Reporting): Core, 4 hours, 50 MCQs + 7 task-based simulations.

- Part 2 – AUD (Auditing and Attestation): Core, 4 hours, 78 MCQs + 7 simulations.

- Part 3 – REG (Taxation and Regulation): Core, 4 hours, 72 MCQs + 8 simulations.

- Part 4 – Your Discipline: pick one of BAR, ISC or TCP. 4 hours.

The structure is the same whether you sit in Delhi or Denver, so an Indian candidate prepares for exactly the same paper as anyone else. This article walks through each part and if you want the wider picture afterwards, our full US CPA course details page covers eligibility, fees and timelines.

How the Four-Part Model Came About

For years the CPA Exam ran on four equal papers, one of which was the old BEC section. That changed in January 2024, when the AICPA and NASBA rolled out a redesign called CPA Evolution. The logic was simple enough: a CPA auditing IT systems does not use the same toolkit as one writing complex tax returns, so why test them on an identical fourth paper?

Under the new design, BEC was retired. In its place came a “Core plus Discipline” model: three sections every candidate must clear and one specialised section the candidate selects. The 2026 exam still runs on this exact framework, with no parts added or reshuffled since the launch. If you trained on the older pattern, the change worth remembering is that there is no longer an easy confidence-builder paper; each part now carries real weight.

Part 1 – Financial Accounting and Reporting (FAR)

FAR is where most people begin and it is widely regarded as the heaviest of the three Core papers. The section checks whether you genuinely understand US GAAP, can put together and read financial statements and know how accounting works for state and local governments as well as not-for-profit bodies. Memorising definitions will not carry you through. The exam is built to see whether you can apply concepts under pressure.

A few questions in each part are unscored “pretest” items being trialled for future exams, though you will not know which ones, so treat all of them seriously.

The AICPA Blueprints divide FAR into these areas:

- Conceptual framework and financial reporting

- Select financial statement accounts

- Select transactions

- State and local government accounting

FAR has historically posted one of the lower pass rates among the Core sections. The breadth of material is usually blamed and that breadth is exactly why a structured study plan matters more here than anywhere else.

Part 2 – Auditing and Attestation (AUD)

AUD tests your grasp of the audit process from start to finish: planning an engagement, weighing risk, gathering evidence and reaching a defensible conclusion. Professional ethics and independence run through the whole section. One quirk sets this paper apart: AUD is the only section that probes the highest reasoning skill, evaluation, which is part of why many candidates find its questions slippery. More than one option can look correct until you read closely.

You get four hours. The simulations sit in the final three testlets. As with FAR, a handful of items are unscored pretest questions.

The AICPA Blueprints break AUD into four areas:

- Ethics, professional responsibilities and general principles

- Assessing risk and developing a planned response

- Performing further procedures and obtaining evidence

- Forming conclusions and reporting

Because the paper leans heavily on theory and judgement rather than calculation, candidates often describe the difficulty as a matter of reading carefully rather than crunching numbers.

Part 3 – Taxation and Regulation (REG)

REG covers US federal taxation alongside business law and professional ethics. Individual tax, entity tax, property transactions and the legal duties of a practitioner all sit inside this section. For an Indian candidate with no prior exposure to the US tax code, this is often the part that demands the most fresh learning, since little of it overlaps with Indian taxation.

The format mirrors the other Core papers: four hours, with 72 multiple-choice questions and 8 task-based simulations, scored on a 50-50 split. The MCQs are spread across two testlets of 36 each.

REG is mapped across these areas in the Blueprints:

- Ethics, professional responsibilities and federal tax procedures

- Business law

- Federal taxation of property transactions

- Federal taxation of individuals

- Federal taxation of entities, including tax preparation

Part 4 – The Discipline Section: BAR, ISC or TCP

Here is where you make your one real choice. Every candidate clears the same three Core papers but the fourth is yours to select and it should reflect where you want your career to go. You only sit one of the three. Once you are licensed you can practise in any area regardless of which Discipline you picked, so the decision shapes your study, not your future scope.

A practical note on scheduling before we look at each option: the Core sections are offered through continuous testing across the year but the Discipline sections open only in fixed quarterly windows. That makes the timing of your fourth paper something you plan around, not something you book on a whim.

Business Analysis and Reporting (BAR)

BAR extends FAR. It digs into financial statement analysis, technical accounting matters such as revenue recognition and leases and reporting requirements for government entities. If FAR was your strongest Core paper, BAR is the natural follow-on, since much of the ground is shared. The paper carries 50 MCQs and 7 simulations, weighted 50-50, over four hours. Candidates eyeing roles in financial reporting, planning or analysis tend to land here.

Information Systems and Controls (ISC)

ISC is the technology-facing Discipline and grows out of AUD. It covers IT audit and advisory work, data management, system security and privacy and SOC engagements. Its structure differs from the other two in a way worth noting: ISC carries 82 MCQs and 6 simulations and the weighting is 60% MCQs to 40% simulations rather than the usual even split. Candidates heading toward IT audit, cybersecurity or data roles usually choose it.

Tax Compliance and Planning (TCP)

TCP is the tax specialisation, built on top of REG. It goes deeper into individual and business tax compliance, personal financial planning and property transactions, including thornier areas like transactions between a business and its owners. The format is 68 MCQs and 7 simulations, weighted 50-50, across four hours. It has been the strongest-scoring Discipline since CPA Evolution began. Future tax advisers, consultants and planners gravitate toward it.

The Four Parts Side by Side

| Part | Section | Type | Duration | MCQs | Simulations | Weighting |

| 1 | FAR | Core | 4 hours | 50 | 7 | 50/50 |

| 2 | AUD | Core | 4 hours | 78 | 7 | 50/50 |

| 3 | REG | Core | 4 hours | 72 | 8 | 50/50 |

| 4 | BAR | Discipline | 4 hours | 50 | 7 | 50/50 |

| 4 | ISC | Discipline | 4 hours | 82 | 6 | 60/40 |

| 4 | TCP | Discipline | 4 hours | 68 | 7 | 50/50 |

What the Exam Day Itself Looks Like

Each part is computer-based and runs at a Prometric centre. The four-hour clock is the testing time but you should budget extra minutes at both ends. Before the exam starts, two welcome screens ask you to confirm details and enter your launch and confidentiality codes, five minutes each. After your third testlet you are offered a standardised 15-minute break that pauses the timer and it is the only break that does. Other breaks are allowed but the clock keeps running through them. A short survey closes things out once you finish.

Two question types run through every part. Multiple-choice questions give you four options each and test recall and quick reasoning. Task-based simulations are interactive case studies that ask you to apply what you know to a realistic scenario and because they contain several responses, partial credit is on the table. That partial-credit detail is easy to overlook, yet it rewards attempting every sub-part of a simulation rather than leaving blanks.

What Changes for Candidates Sitting in India

The paper is identical the world over, so nothing about the four-part structure shifts when you test in India. The differences are administrative and they are worth knowing before you commit:

- Credit evaluation. A US state board needs your Indian degree translated into US credit hours. This is done through an approved evaluation agency and it typically takes several weeks, so it pays to start early.

- The 150-credit rule. Most states want 150 US-equivalent credits for licensure. A standard three-year Indian bachelor’s degree often falls short, which is why many candidates pair it with a master’s or a professional qualification.

- International testing fee. Sitting the exam at an Indian Prometric centre carries an extra fee per section on top of the standard exam fee. It is cheaper than flying to the US but it does push up the total and the figure is revised from time to time.

- Test centres. The exam runs in cities including New Delhi, Mumbai, Hyderabad, Bangalore, Chennai, Ahmedabad, Kolkata and Thiruvananthapuram. You book through Prometric once your Notice to Schedule comes through.

For Indian Chartered Accountants in particular, the overlap with FAR and AUD often makes the Core papers feel familiar, while REG and a tax Discipline call for genuinely new study. You can compare or see the full course fee on our CPA course fees page.

Putting the Order Together

Since the Discipline papers open only in fixed windows while the Core papers run year-round, a sensible plan often pairs a Discipline with the Core section that feeds it. Sit FAR then BAR or AUD then ISC or REG then TCP, so the related material is still fresh when you reach the fourth part. There is no rule forcing this and plenty of candidates start with whatever they feel readiest for. What matters is that the order is deliberate and tuned to your own strengths and to the rolling time window your state board allows.

Frequently Asked Questions

Four. Three are fixed Core sections, FAR, AUD and REG, that everyone takes. The fourth is a Discipline section you choose from BAR, ISC or TCP.

The exam itself is identical. The content, the four parts, the question types and the four-hour length do not change. What differs is the logistics around it: credit evaluation through NASBA, an international testing fee per section and booking a slot at a Prometric centre inside India.

There is no universally right answer. FAR is a common opener because it underpins so much of the rest but starting with your freshest subject works too. Pairing a Discipline with its related Core section is a popular tactic.

A rolling window starts once you clear your first part. NASBA now recommends 30 months, though the exact figure is set by your state board, so confirm it with the jurisdiction you apply through.

A Final Word

Knowing the structure before you start studying saves a surprising amount of grief. Three Core papers test the common ground every CPA stands on, the fourth lets you lean into the work you actually want to do. Map your four parts against your strengths and your state board’s window, prepare each one properly and the path to the licence becomes a series of clear steps rather than a guessing game. If you would like that path mapped out for you, the US CPA course at VG Learning Destination pairs Gleim study material with faculty who have sat these papers themselves.